Watch out for card skimming at the gas pump

77 skimmers found in Arizona so far this year

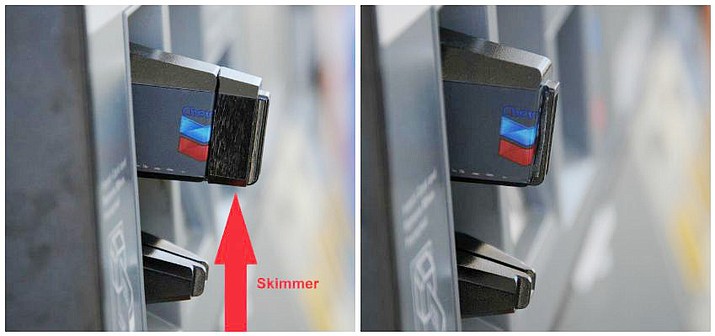

Some credit card skimmers can be placed on the exterior of a credit card reader. (Arizona Weights and Measures Services Division/Courtesy)

To view this content you must be logged in as a subscriber.

Already have a digital account? Log in here

4 WEEKS

$12.50

UNLIMITED

DIGITAL ACCESS

4 WEEKS

52 WEEKS

$135

UNLIMITED

DIGITAL ACCESS

FOR 52 WEEKS

DAY PASS

$2.00

UNLIMITED

DIGITAL ACCESS

FOR 24 HOURS

Plans include full website access, e-Edition and exclusive online

extras.

Print and Digital combo plans also available.

ALREADY A PRINT SUBSCRIBER?

Sign up for our e-News Alerts

Most Read

SUBMIT FEEDBACK

Click Below to: